Fraud detection systems are built to protect businesses, but when they wrongly flag genuine customers, the problem becomes expensive. For Canadian fintech companies, banks, payment platforms, insurance providers, and eCommerce businesses, false positives can lead to failed transactions, manual reviews, support tickets, and poor customer experience.

Digital fraud remains a serious concern for Canadian businesses, especially as more payments, onboarding, lending, and insurance interactions move online. The challenge is not only catching fraud. It is doing so accurately, quickly, and responsibly.

This is where machine learning in fraud detection becomes valuable. Instead of depending only on fixed rules, machine learning helps systems understand context, learn from historical patterns, and reduce false positives in fraud detection while supporting stronger security.

What Are False Positives in Fraud Detection?

A false positive in fraud detection is when a genuine customer activity is wrongly flagged as fraud.

This can happen when a real customer makes a high-value purchase, logs in from a new device, travels to another location, submits a genuine insurance claim, or makes an unusual but legitimate payment. The system treats the activity as suspicious, even though the customer is real.

False positives are not just technical errors. They affect customer trust, payment approval rates, support workload, and fraud team productivity.

Why False Positives Are a Serious Business Problem

When fraud detection systems over-flag genuine activity, the impact moves beyond one blocked transaction. A customer may get declined, contact support, wait for manual review, and eventually lose confidence in the platform.

For businesses handling thousands of transactions, this creates a larger operational problem. Payment approval rates may drop, support tickets increase, fraud teams spend more time checking harmless alerts, and customer experience suffers.

For companies trying to reduce false positives in fraud detection, the goal is clear: catch real fraud without punishing genuine users. AI fraud detection built with machine learning supports this by making fraud decisions more contextual and accurate.

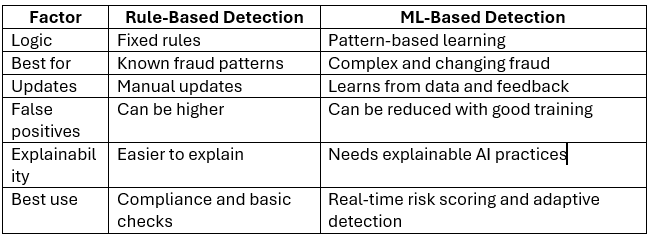

Why Rule-Based Fraud Detection Creates Too Many False Alerts

Traditional fraud detection systems often work with fixed rules. For example, they may flag transactions above a certain amount, logins from new locations, repeated payment attempts, or international purchases.

These rules are useful for known fraud patterns and compliance checks. However, they often miss context. A customer may spend more than usual because of a special occasion. A business owner may make multiple payments in a short time. A traveler may log in from different countries.

Rule-based fraud detection still has value, but relying only on rules can create unnecessary alerts. A better approach is to combine rules with machine learning models that can understand behaviour, context, and risk levels.

How Machine Learning Reduces False Positives in Fraud Detection

Machine learning improves fraud detection by studying patterns instead of judging every transaction through fixed conditions. It looks at multiple signals together and supports better decision-making in real time.

Behaviour-Based Customer Analysis

Machine learning compares current activity with a customer’s normal behaviour. It studies typical transaction amounts, login times, devices, locations, merchant types, and purchase frequency.

This customer behavior analysis helps the system understand whether an unusual action is actually risky or simply different from average behaviour. As a result, genuine customers are less likely to be blocked unnecessarily.

Fraud Risk Scoring Instead of Direct Blocking

Instead of making only approve-or-block decisions, ML systems assign a fraud risk scoring value to each activity. Low-risk transactions can be approved automatically. Medium-risk activity can trigger extra verification. High-risk cases can be sent for manual review.

This layered approach helps businesses reduce unnecessary declines while still protecting against suspicious activity.

Real-Time Transaction Context

Modern fraud systems need to act quickly. Real-time fraud detection uses signals such as transaction amount, time, device, IP location, account history, merchant category, and payment method.

A transaction may look risky based on one factor, but when all signals are checked together, it may be safe. Machine learning helps make that distinction faster and more accurately.

Anomaly Detection Without Overblocking

Anomaly detection helps identify unusual behaviour. However, good ML models do not treat every anomaly as fraud. They weigh unusual activity against other signals before escalating it.

It is important to be realistic. Machine learning can help reduce false positives when models are properly trained, tested, monitored, and updated. It does not eliminate false positives completely.

Learning From Fraud Analyst Feedback

Fraud teams play an important role in improving ML systems. When analysts mark alerts as genuine or fraudulent, that feedback helps the model improve over time.

This human-in-the-loop process makes AI fraud detection more practical because the system learns from real decisions made by experienced fraud professionals.

Machine Learning vs Rule-Based Fraud Detection

The best fraud detection systems often use both approaches. Rules handle clear compliance needs, while machine learning supports adaptive fraud detection and better risk decisions.

Industry Use Cases for Canadian Businesses

False positives affect different industries in different ways, but the business goal remains the same: reduce risk without blocking genuine users.

In banking and credit unions, ML can help reduce false card declines and unnecessary transfer alerts. For fintech and payment platforms, it supports wallet payments, KYC checks, onboarding, and transaction monitoring. In insurance, ML can identify suspicious claims while reducing delays for genuine policyholders.

eCommerce businesses can use ML to reduce fake orders, account takeover risk, refund abuse, and payment declines. Lending platforms can use it to review borrower applications, identify unusual patterns, and make faster risk decisions.

Each industry has different fraud risks, but the core requirement is the same: protect the business without creating friction for genuine customers.

What Data Helps ML Reduce False Positives?

The quality of ML fraud detection depends heavily on the quality of data. Useful data may include transaction history, login behaviour, device fingerprints, IP and location signals, customer profile data, merchant category, payment method, chargeback history, failed payment attempts, and fraud analyst feedback.

Clean, well-labelled data is important because poor data can lead to poor model decisions. Customer behavior analysis and fraud risk scoring both depend on accurate historical data.

This is why data preparation is as important as model development in any machine learning in fraud detection project.

Cloud Architecture for Real-Time Fraud Detection

Real-time fraud detection requires more than a good ML model. It needs fast data pipelines, secure storage, API integrations, model deployment, monitoring dashboards, and scalable infrastructure.

Cloud environments are useful for fraud detection because they support elastic scaling, secure data workflows, and continuous deployment. Businesses building or upgrading fraud systems can benefit from cloud consulting services in Canada to design reliable architecture for real-time scoring, monitoring, and compliance-ready operations.

This section is especially important for fintech, banking, insurance, and payment platforms where speed, security, and uptime matter.

Compliance, Privacy, and Explainability in AI Fraud Detection

For Canadian businesses, AI fraud detection should be designed with privacy, security, and explainability in mind. Fraud systems should include audit logs, access controls, bias monitoring, model documentation, and human review for high-risk cases.

Compliance teams need to understand why a transaction was flagged. A fraud risk score is more useful when it comes with a reason, such as unusual device, new location, irregular payment amount, or suspicious account behaviour.

Canadian businesses should design AI fraud detection systems with privacy, auditability, and explainability in mind. This may include PIPEDA-aligned data handling, FINTRAC-aware monitoring workflows, access controls, audit logs, bias checks, and human review for high-risk decisions. Machine learning should support compliance, not replace proper governance.

Business Benefits of Reducing False Positives

Reducing false positives can create practical business benefits for Canadian financial and digital commerce businesses. When genuine transactions are approved faster, companies can improve payment approval rates, reduce unnecessary declines, lower support ticket volume, and create smoother customer experiences.

ML-based fraud detection also helps fraud teams work more efficiently. Instead of reviewing every unusual transaction manually, analysts can focus on high-risk cases that need deeper investigation. This can support faster fraud review, better team productivity, and more consistent decision-making.

The benefits depend on transaction volume, data quality, model accuracy, and continuous monitoring. Machine learning can improve fraud decisioning, but it should be implemented with proper testing, explainability, analyst feedback, and compliance review.

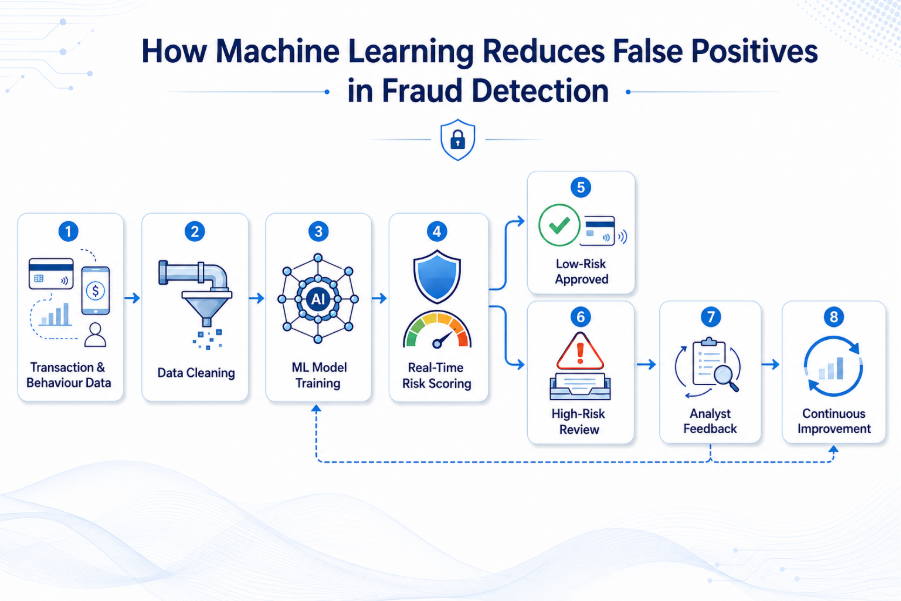

Simple Workflow: How ML Reduces False Positives

Here is a simple workflow showing how machine learning reduces false positives in fraud detection:

- Collect transaction and customer behaviour data

- Clean and prepare labelled fraud datasets

- Train ML models on genuine and suspicious patterns

- Assign real-time fraud risk scores

- Approve low-risk actions automatically

- Send high-risk cases for fraud review

- Capture analyst feedback

- Improve the model continuously

Figure: How machine learning improves fraud risk scoring and reduces false positives

This feedback loop helps businesses move from static rules to smarter fraud decisioning.

Why Choose Theta Technolabs?

Theta Technolabs helps businesses build custom AI and ML-powered digital solutions for fraud detection, risk scoring, automation, and secure cloud-based operations. The company’s capabilities include machine learning model development, AI fraud detection systems, fraud risk scoring engines, API integrations, cloud architecture, and dashboards for fraud and compliance teams.

For fintech, banking, insurance, lending, and eCommerce teams, Theta Technolabs offers practical technology support across web, mobile, and cloud.

Conclusion

False positives are a real business problem. They create failed transactions, manual reviews, customer frustration, and operational pressure. Rule-based systems alone may not be enough to handle modern fraud patterns, especially for businesses operating at scale across digital channels.

Machine learning supports better fraud accuracy through behaviour analysis, risk scoring, anomaly detection, real-time context, and feedback learning. For Canadian fintech, banking, payment, insurance, lending, and eCommerce businesses, these capabilities can reduce fraud friction, protect genuine customers, and improve operational efficiency.

With the right machine learning services, businesses can build smarter fraud detection systems that improve risk decisions and create smoother digital experiences for genuine customers.

Ready to Build a Smarter Fraud Detection System?

Looking to build an AI-powered fraud detection system for your fintech, banking, insurance, payment, lending, or eCommerce platform?

Theta Technolabs can help you design secure, scalable, and cloud-ready solutions using web, mobile, cloud, and machine learning expertise. Whether you are starting from scratch or upgrading an existing system, our team can help you build practical fraud detection solutions that balance security with customer experience.

Connect with us at sales@thetatechnolabs.com.

Frequently Asked Questions

1. What is a false positive in fraud detection?

A false positive in fraud detection occurs when a genuine customer action, such as a payment, login, or claim, is wrongly identified as suspicious or fraudulent.

2. How does machine learning reduce false positives in fraud detection?

Machine learning reduces false positives by using customer behavior analysis, fraud risk scoring, anomaly detection, and historical patterns to make better fraud decisions.

3. Is machine learning better than rule-based fraud detection?

Machine learning is more adaptive, but rule-based fraud detection is still useful for known patterns and compliance checks. A hybrid approach often works best.

4. Can machine learning support real-time fraud detection?

Yes. ML models can support real-time fraud detection when they are connected to fast data pipelines, secure cloud infrastructure, and optimized scoring systems.

5. What data is needed for AI fraud detection?

AI fraud detection may use transaction history, device data, login behaviour, location signals, merchant details, payment methods, and fraud analyst feedback.

6. Is AI fraud detection useful for Canadian businesses?

Yes. These solutions help Canadian financial and digital commerce businesses improve fraud accuracy, reduce false alerts, and protect genuine users.